A real estate bubble is a complex economic phenomenon characterized by rapid and unjustified surges in property prices, often followed by sharp corrections or market crashes. In the volatile global economic landscape of 2026, gaining a deep understanding of how these bubbles form is essential for protecting capital and achieving sustainable investment growth.

At Binaa Investment, as international real estate advisory experts, we rely on data-driven analysis and insights from leading global financial institutions to deliver clarity and confidence to our clients. In this comprehensive report, we explore the dynamics of real estate bubbles, identify key warning indicators, and outline strategic approaches to redirect investments toward fundamentally strong and resilient markets—such as Istanbul and Dubai.

While a real estate bubble can offer short-term gains, it also poses significant risks. A housing market crash can lead to financial losses and economic downturns. Recognizing the signs of a bubble is essential for making informed investment decisions.

Investors should focus on long-term strategies to mitigate risks. Diversifying investment portfolios can also help. Monitoring economic indicators and understanding local market dynamics are key to avoiding pitfalls.

Government policies and regulations play a role in bubble formation. They can either exacerbate or mitigate the effects. Educating yourself about market trends and seeking professional advice can be invaluable.

The psychological aspect of market speculation often fuels bubbles. Media and public perception can amplify these effects. Sustainable investing practices can contribute to a more stable market.

In this article, we will explore the intricacies of the real estate bubble. We will discuss its advantages, disadvantages, and strategies to avoid investment risks.

What Is a Real Estate Bubble?

A real estate bubble happens when property prices rise quickly and unsustainably. It’s driven by high demand, speculation, and sometimes economic growth. Initially, this creates a sense of abundance and opportunity.

A bubble forms when buyers, motivated by rapidly increasing prices, continue to invest. This drives demand even further. Such enthusiasm is often based more on emotion than financial rationality.

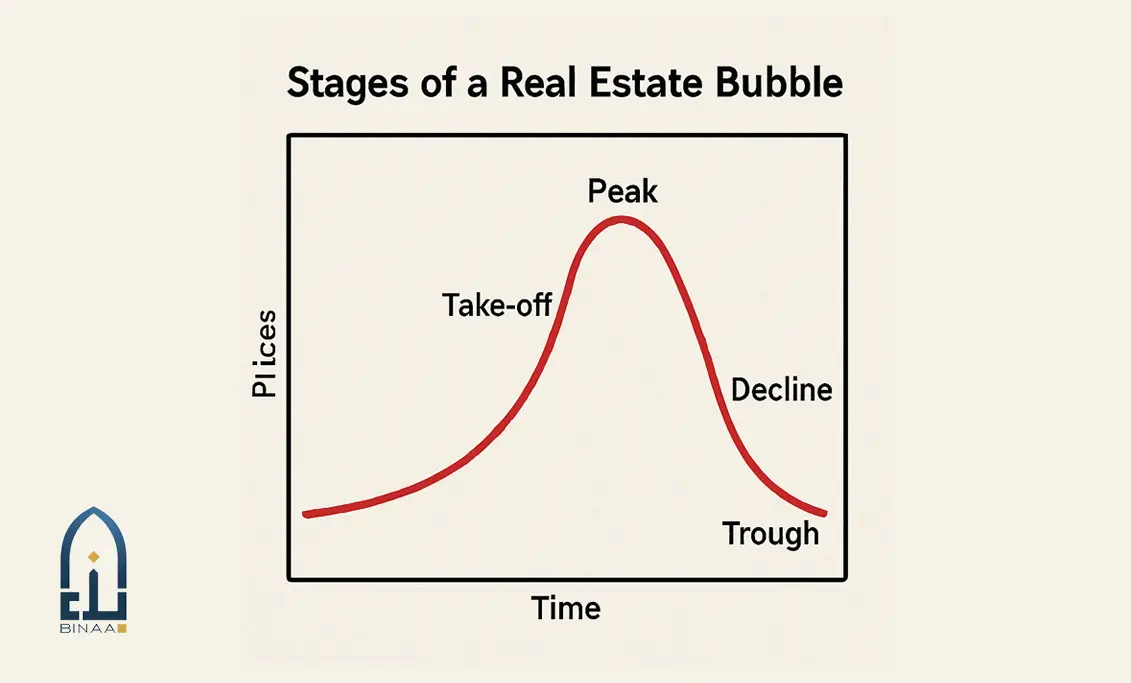

However, these price increases are not sustainable. They diverge from the actual economic fundamentals of the market. Eventually, prices reach a peak and start to decline, leading to a market correction.

Several factors contribute to the formation of a real estate bubble. These include:

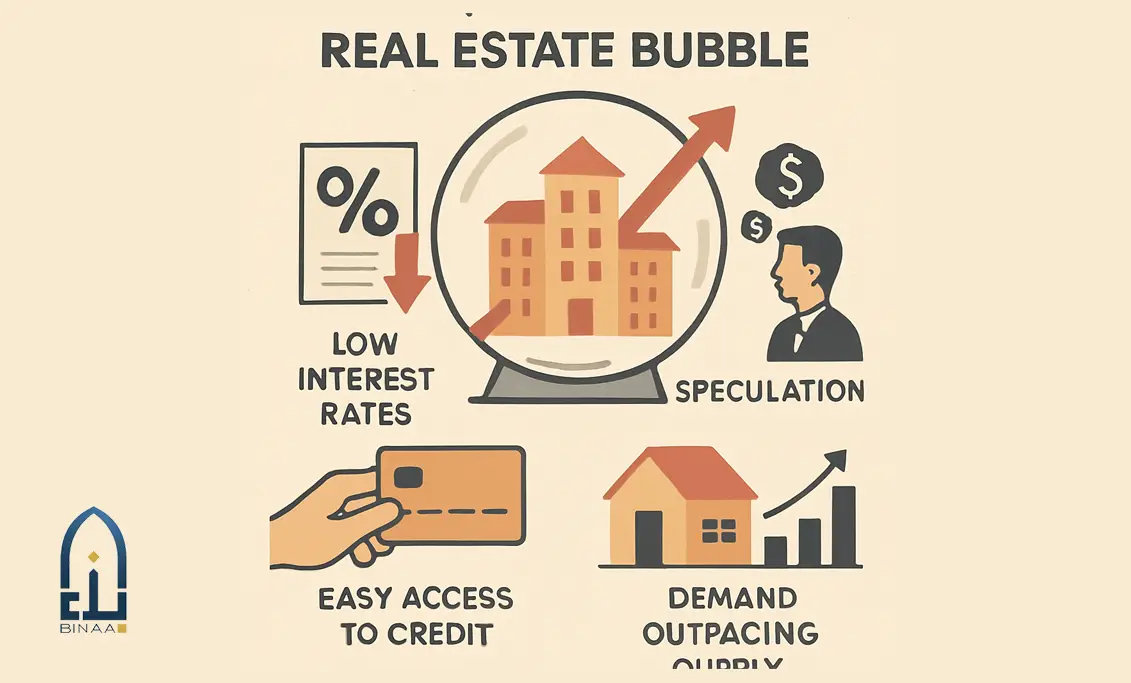

- Low interest rates encouraging borrowing.

- Easy access to credit.

- High levels of speculative buying.

When a bubble bursts, it can lead to significant negative outcomes. The market may experience a sharp decline, causing financial hardships. This is particularly severe for those who bought properties at inflated prices.

Understanding a real estate bubble requires recognizing the gap between pricing and market fundamentals. When the gap widens significantly, a bubble may be forming. Investors and buyers alike must be aware of these signs to avoid potential losses.

How Do Real Estate Bubbles Form?

Real estate bubbles start with a mix of economic conditions and market behaviors. Initially, favorable conditions spark increased demand for properties. Low interest rates play a significant role by making loans cheaper and more accessible.

Credit availability further amplifies the situation. When banks offer easy credit, more people can buy homes, inflating demand. This results in rapidly increasing property values.

Speculation also drives a bubble. Investors purchase properties with the belief they’ll sell for a higher price later. This “buy-low-sell-high” mentality can stimulate short-term investments.

Market psychology contributes to the bubble's growth. Buyers often see rising prices and fear missing out. This fear of missing out leads to rushed decisions and overvaluation.

Key elements in bubble formation include:

- Low interest rates and easy credit.

- Speculative buying with little regard for risks.

- Overconfidence in continually rising prices.

- Psychological factors like market enthusiasm and fear of missing out.

These bubbles can also be influenced by broader economic factors. Economic growth, government incentives, and population increases can further fuel demand. However, these same factors, once reversed, can trigger the bubble to burst.

Therefore, it’s crucial to remain cautious during periods of rapid price increases. Identifying the underlying factors and recognizing the signs can prevent steep financial losses. By understanding how bubbles form, stakeholders can better prepare and react.

Historical Examples of Real Estate Bubbles

Real estate bubbles have appeared throughout history, leaving a trail of financial turmoil. One infamous example is the U.S. housing bubble of the mid-2000s. This bubble was characterized by overly optimistic home prices driven by lenient lending practices.

Another example is Japan's asset price bubble during the late 1980s. Driven by rapid economic growth and speculative investment, property prices soared but eventually collapsed. This led to a prolonged economic downturn known as the Lost Decade.

In Europe, the Spanish housing bubble provides another case. From the late 1990s into the mid-2000s, Spain experienced a building boom. When the bubble burst, it resulted in significant economic distress.

These historical bubbles share common attributes:

- Excessive speculation.

- Easy access to credit.

- Overinflated property values.

- Subsequent economic downturns.

The consequences of these bubbles extend beyond the immediate financial domain. For instance, they often lead to broader economic repercussions, affecting sectors like banking and construction. Each bubble leaves a unique imprint on the housing and employment markets.

Understanding these past events is crucial for current investors and policymakers. By analyzing the triggers and outcomes, future bubbles might be anticipated and mitigated. This historical perspective highlights the cyclical nature of real estate markets.

Overall, while the specifics may vary, the underlying causes of these bubbles often resemble each other. This knowledge serves as a cautionary tale, reminding investors of the potential risks involved. Keeping an eye on market behaviors and economic indicators can help in avoiding similar pitfalls.

Key Signs and Indicators of a Real Estate Bubble

Spotting a real estate bubble before it bursts can save investors significant losses. One of the primary indicators is the rapid escalation of property prices, often outpacing income growth. When properties become unaffordable, it signals a potential bubble.

Increased speculative buying is another red flag. If buyers are purchasing properties primarily for investment, not for residence, caution is warranted. This behavior often fuels unsustainable price hikes.

Debt levels are also a crucial indicator. When there is an increase in mortgages with high loan-to-value ratios, it suggests a riskier market. Easy access to credit can encourage excessive borrowing, inflating the bubble further.

Look out for a surge in construction and development projects. When developers flood the market with new properties, it can lead to oversupply. This often happens when demand is artificially high, further distorting the market.

- Rapidly rising property prices.

- Surge in speculative buying.

- High levels of consumer debt.

- Overwhelming supply of new constructions.

Monitoring economic indicators such as interest rates and employment levels provides additional insights. Low interest rates often contribute to bubbles by making borrowing cheaper. Conversely, high unemployment can reduce demand, exposing overvalued markets.

Public sentiment and media hype can amplify bubble conditions. If media frequently praises the housing market's "endless" growth, skepticism is advisable. This enthusiasm can drive irrational investment behaviors.

Recognizing these signs can help investors make informed decisions. It's crucial to remain vigilant and approach the real estate market with caution. Being aware of these indicators can mitigate the risk of falling into the trap of a real estate bubble.

Advantages of a Real Estate Bubble

Real estate bubbles, despite their risks, offer certain advantages to specific market players. One significant benefit is the potential for short-term financial gains. Investors who purchase properties early in the cycle often see substantial returns when selling at peak prices.

During a bubble, economic activity often boosts. As property values rise, homeowners may perceive increased wealth, leading to higher consumer spending. This perceived wealth effect can benefit local businesses and service providers.

Bubbles frequently encourage development and infrastructure expansion. Construction companies and related industries often see increased demand for their services. This, in turn, can create more jobs, benefiting local economies.

Additionally, governments may benefit from rising property tax revenues. As property values increase, so do the taxes, filling public coffers. This additional revenue can support community projects and improvements.

- Short-term financial gains.

- Boost in local economic activity.

- Increased demand for construction services.

- Higher property tax revenues.

Despite these benefits, it's essential to note that they are typically short-lived. The advantages are mainly for those who can act quickly and exit before the bubble bursts. As such, prudent investors should remain aware of the broader market dynamics to capitalize on these temporary benefits without being caught when the bubble eventually deflates.

Disadvantages and Investment Risks of a Real Estate Bubble

While real estate bubbles can offer short-term gains, they also bring significant downsides. A primary concern is the high risk of a housing market crash. When the bubble bursts, property values can plummet rapidly, erasing gains.

This sudden crash results in financial turmoil for investors and homeowners. Many may find themselves with properties worth less than their purchase price. This phenomenon, known as being "underwater," poses serious financial challenge.

The broader economy can suffer too. A crash can lead to increased foreclosures, hurting individuals and communities alike. As homes are foreclosed, neighborhoods may witness deteriorating property conditions, affecting overall market stability.

Investment risks are also highlighted in these environments. Market speculation becomes rampant, fueling price discrepancies and unsustainable growth. Many investors may make decisions based on hype rather than sound financial analysis.

Additionally, the aftermath of a bubble can lead to stricter lending practices. Financial institutions, in efforts to mitigate their losses, might tighten credit standards. This shift can make it more difficult for prospective buyers to secure financing.

Economic downturns may follow a burst, with impacts reaching various sectors. Construction, banking, and retail often experience ripple effects. The loss of equity and confidence can dampen consumer spending, affecting GDP.

- Risk of housing market crash

- Potential for homeowners to be "underwater"

- Increased foreclosures and community impacts

- Economic ripple effects across sectors

- Stricter lending and credit practices

Understanding these disadvantages helps investors prepare better. Avoiding the pitfalls requires careful market analysis and a focus on long-term strategies. By doing so, investors can navigate uncertain markets with greater confidence.

The Housing Market Crash: What Happens When the Bubble Bursts?

A housing market crash can have far-reaching consequences. When a real estate bubble bursts, it leads to a sharp and rapid decline in property prices. This sudden drop creates financial chaos for homeowners and investors alike.

Homeowners may face negative equity, where their mortgage exceeds their home's value. This situation can result in increased foreclosures, as owners can no longer afford their mortgage payments. Foreclosures, in turn, can flood the market with discounted properties, pushing prices even lower.

The impact extends beyond just property owners. Banks and financial institutions suffer losses due to unpaid loans. This can result in a tightening of credit, making it hard to obtain mortgages or refinance existing ones.

Job losses may occur, particularly in industries closely tied to real estate. Construction jobs decrease as new projects are halted. Retail and service sectors can also feel the pinch as consumer spending declines.

The psychological impact should not be underestimated. A market crash often erodes consumer confidence, affecting other economic areas. People may cut back on spending, saving more due to fears of an uncertain future.

- Sharp decline in property prices

- Increased foreclosures and market flooding

- Tightened credit conditions

- Job losses in construction and related sectors

- Decreased consumer confidence and spending

In summary, a housing market crash can devastate individual finances and the broader economy. Its effects are wide-ranging, influencing everything from banking to employment. Understanding these dynamics can help individuals and investors prepare for and potentially mitigate these impacts.

How to Spot a Real Estate Bubble: Practical Tips

Recognizing a real estate bubble early can prevent financial losses. The signs may not always be obvious, but some key indicators can help. By keeping an eye on these signals, investors and homebuyers can avoid the pitfalls of a bursting bubble.

One important indicator is rapidly increasing property prices. If prices soar beyond income growth or local economic growth, this could indicate a bubble. It's crucial to compare price growth with other economic metrics.

Another sign is speculative buying. When people purchase homes primarily to sell quickly for profit, it suggests speculation is rife. This behavior can drive prices to unsustainable heights.

High levels of debt in the real estate market also signal trouble. If individuals or developers heavily rely on borrowing, the risk of default increases, especially if economic conditions worsen.

Government policies promoting easy credit or low interest rates can inflate a bubble. Monitoring policy changes can offer insights into potential market shifts.

- Rapidly rising property prices

- Speculative buying behaviors

- High market debt levels

- Government policy and credit ease

Staying informed and vigilant can help anticipate a real estate bubble. By observing these practical signs, investors can make informed decisions and minimize their exposure to market turbulence.

Strategies to Avoid the Risks of a Real Estate Bubble

Investing in real estate requires strategic planning, especially with the potential risks of a real estate bubble. Certain strategies can help minimize exposure and ensure stability in volatile markets.

First, focus on long-term investment strategies. By prioritizing long-term growth over short-term gains, investors can ride out market fluctuations without major losses.

Diversification is another key strategy. Spread investments across different asset types and geographic locations. This reduces the impact of a downturn in any single market.

Staying informed about economic indicators is crucial. By monitoring interest rates, employment statistics, and housing supply trends, investors can anticipate market changes and adjust strategies accordingly.

Additionally, avoid over-leveraging. Keeping debt levels low minimizes the risk of financial strain if the market turns sour. Invest only what you can afford to lose.

Developing a solid understanding of local market dynamics is vital. Each market behaves differently, influenced by unique factors. Local insights can aid in making prudent investment choices.

- Prioritize long-term strategies

- Diversify investments

- Monitor economic indicators

- Limit leveraging

- Understand local markets

Adopting these strategies can help mitigate the risks associated with a real estate bubble. By focusing on sustainable investment practices, investors can better navigate the complexities of the housing market and safeguard their financial future.

The Role of Government and Policy in Real Estate Bubbles

Government policies significantly shape real estate market trends. Regulatory measures can either curb or contribute to the formation of real estate bubbles. Understanding these roles can help investors predict and respond to market shifts.

For instance, policies that influence interest rates directly affect housing affordability. Low interest rates can spur demand, sometimes fueling bubbles. Additionally, tax policies may encourage or dissuade speculative investment, impacting market dynamics.

Governments can implement specific actions to prevent or mitigate bubbles:

- Tightening lending standards to limit risky borrowing

- Adjusting interest rates to manage demand

- Implementing taxes that deter speculative investments

These measures aim to create a more stable housing market by controlling the factors that lead to bubbles. Informed investors pay close attention to policy changes, anticipating how such shifts might influence the real estate landscape. Understanding government roles empowers them to make better-informed investment decisions.

The Psychological Side: Market Sentiment and Speculation

The psychology of investors plays a vital role in forming real estate bubbles. Market sentiment can drive prices far above actual value. When confidence in ever-rising prices prevails, speculative buying often follows.

Speculative buying occurs when buyers purchase properties to sell quickly for profit. This behavior creates artificial demand. As more investors jump on board, prices continue to rise, often unsustainably.

Key psychological factors in bubble formation include:

- Overconfidence in the market's growth

- Fear of missing out on potential profits

- Herd mentality leading to mass purchases

These psychological drivers can inflate property values quickly. However, once sentiment shifts, the bubble can burst, leading to rapid price declines. Savvy investors recognize these patterns, using them to anticipate potential market corrections. Understanding the psychological aspects of real estate can be crucial for minimizing risks and preventing financial loss.

Technology and Data: Predicting and Understanding Bubbles

The advent of technology has transformed real estate analysis. Big data and AI models now provide insights that were once unavailable. These tools help in predicting potential market shifts.

Data analytics can track various economic indicators in real time. This approach provides an edge in spotting early signs of a bubble. Machine learning algorithms analyze patterns that humans might miss, enhancing prediction accuracy.

Key technological tools include:

- Predictive analytics for market trends

- Algorithms that identify pricing patterns

- Data visualization for understanding complex information

These advancements enable investors to make data-driven decisions. By evaluating trends and patterns, technology aids in understanding bubble dynamics. This understanding can lead to more informed investment strategies, helping mitigate risks. As the industry evolves, leveraging technology becomes essential in navigating the complexities of the real estate market.

Conclusion: Building a Safer Investment Future

Understanding the intricacies of real estate bubbles is vital. A well-informed investor is less likely to fall prey to speculation. This knowledge helps in navigating the real estate landscape with confidence.

Implementing informed strategies reduces exposure to potential risks. Long-term investment approaches often yield more stable returns. Diversifying across different asset types further shields against market volatility.

Being proactive is crucial. Monitoring economic indicators and staying updated on market trends builds resilience. Education in these areas can fortify an investor's ability to make sound decisions.

By leveraging both technological advancements and traditional analysis, a robust future can be secured. This balanced approach ensures a more sustainable and safe investment journey. As the real estate market continues to evolve, staying informed remains the cornerstone of success.

Supply and Demand Balance – Price-to-Rent Ratio – Price-to-Income Ratio – End-User vs. Investor Ratio – Long-Term Price Stability

Geographical Diversification – Focus on Rental Yields – Selecting Strategic Locations – Avoiding Excessive Leverage – Partnering with Expert Advisors such as Binaa Investment

Source